Welcome to the latest instalment of The Buzzword - our new column on the latest pulse and insights of the Malaysian automotive industry, where we aim to educate and discourse on a wide range of automotive topics, all without interference from advertisers and sponsors. The opinions expressed in The Buzzword belong solely to the author; they are not sponsored, nor are they for sale.

Malaysians love their cars (and motorbikes). Based on 2024 data, we have no less than 38.7 million registered vehicles with passenger cars making up over 50% of the total. So when a news report surfaced about BYD – the best-selling EV brand in Malaysia – having second thoughts about producing cars locally, many car-loving Malaysians blew their head gaskets, so to speak.

But with the benefit of time and opportunity to properly digest MITI’s (Ministry of Investment, Trade and Industry of Malaysia) meaty response, we hereby humbly offer our take on the two key issues which arose from the aforementioned news report by The Edge. Peace to the world, here goes.

The ceiling price for CKD BYD models

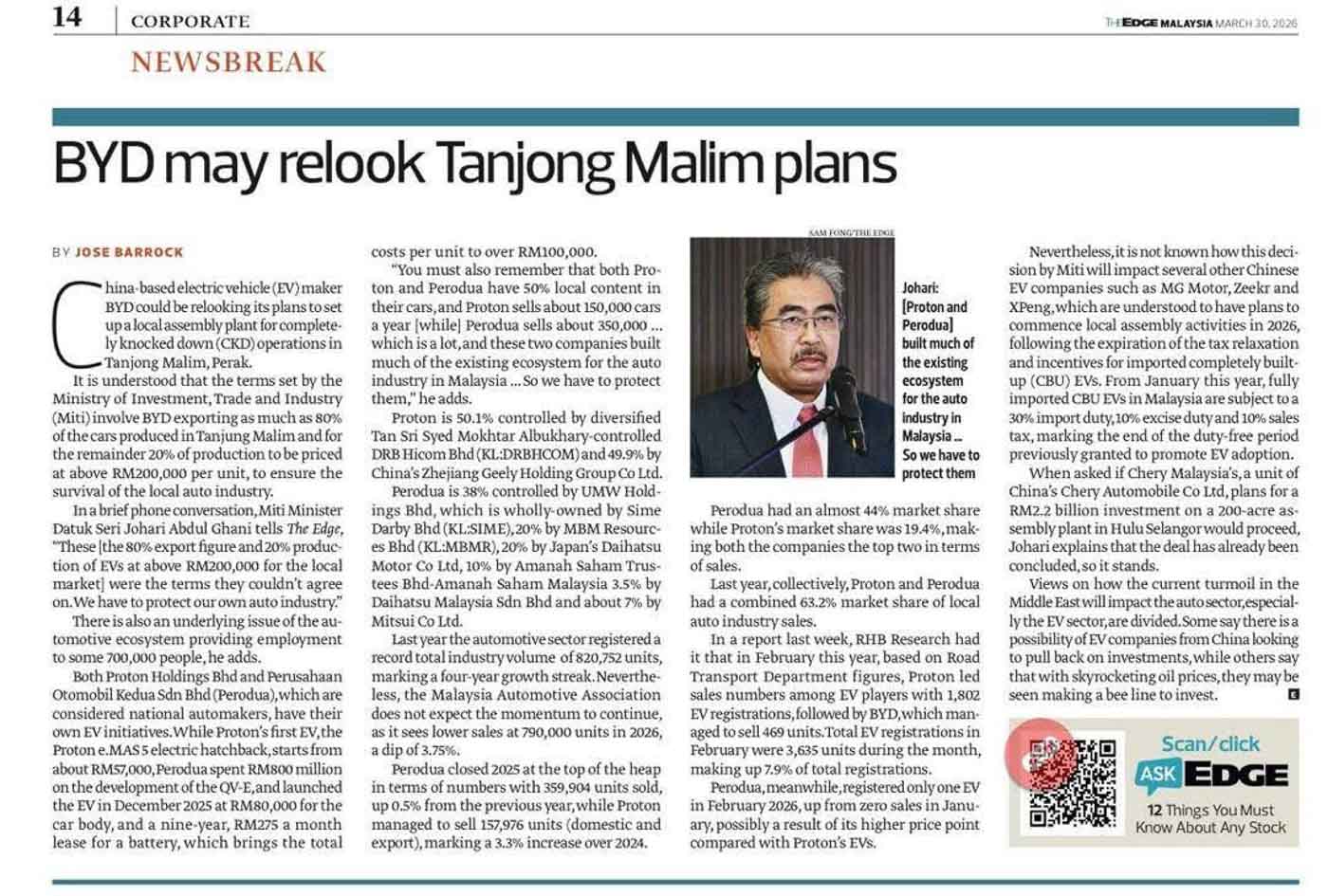

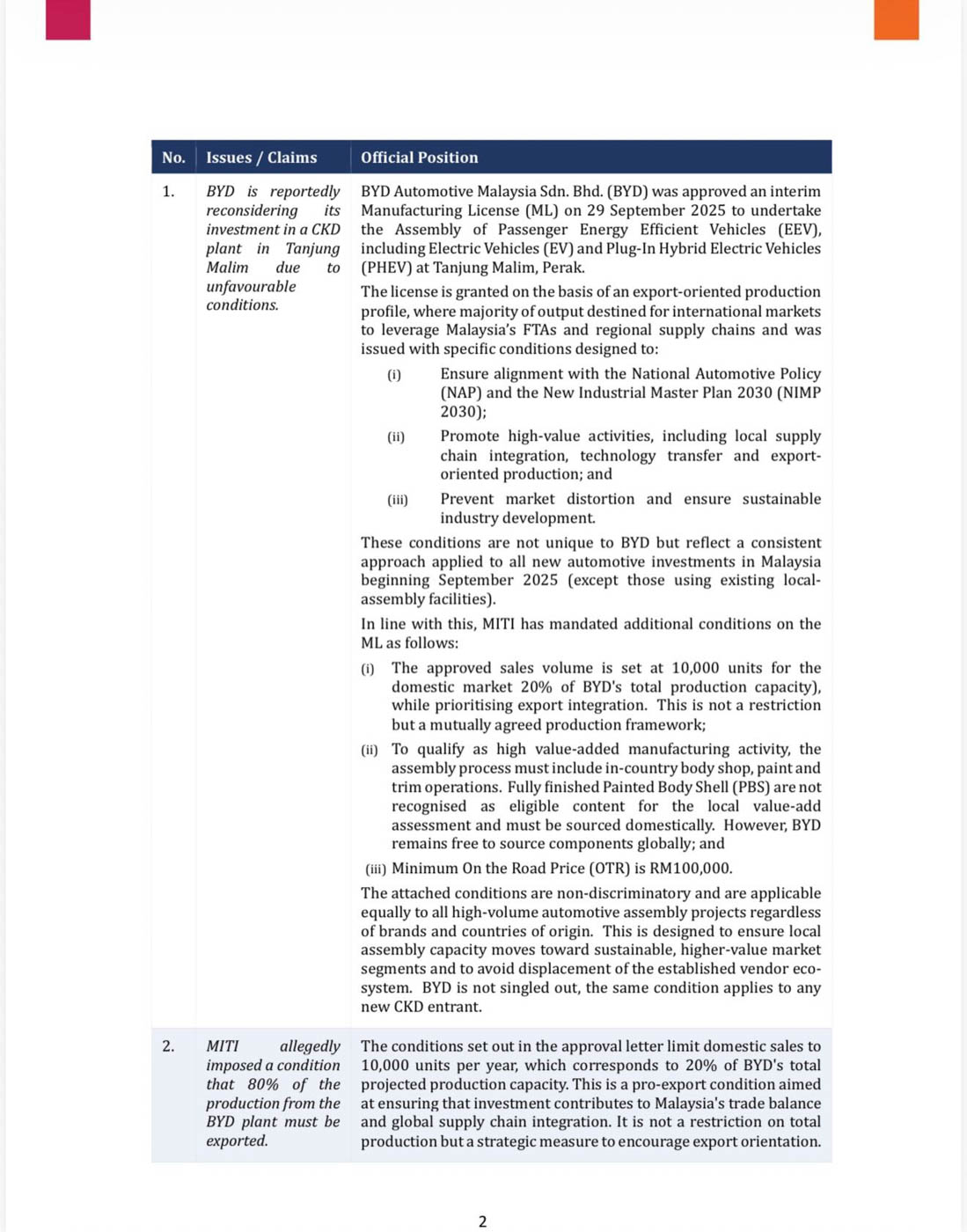

Following the clarification by MITI, the reported floor price of RM200,000 to be imposed on BYD’s model range turned out to be inaccurate (MITI’s word, not ours). Instead, the correct number should have been RM100,000, on-the-road price inclusive of insurance and road tax.

But what does this mean? As wonderful as it may be to visualise an automotive market with zero duties and restrictions, we do not live in a vacuum. The Malaysian market has a unique backdrop other markets in the region don’t have – two established national car brands which dominate over 60% of the market share, comprising mainly affordably priced sub-RM100K models.

According to MITI, the Proton and Perodua ecosystems employ over 700,000 people, producing cars with over 70% local content. Yes, protectionist policies being applied to potential investors are paradoxical, but the automobile industry is also undergoing a generational shift, and such curbs can partially cushion the existing ecosystem from being upended by cutthroat price wars seen in the Chinese domestic market.

In so doing, car buyers here could conceivably miss out on BYD’s most affordable BEV, the Seagull supermini, but given that BYD’s global line up feature more higher value models, maybe we aren’t missing out that much.

Having said that, there’s the avenue of utilising existing CKD plants to assemble models priced below RM100K (Sime Motors’ Kulim plant is an option). This isn’t without precedent as the TQ Wuling Bingo which starts from RM63,000, is assembled at Tan Chong Motor’s Segambut plant. So don’t rule out a sub-RM100K BYD CKD model just yet.

While the RM100,000 floor price may not sit well with the notion of a free, unfettered market, the influx of Chinese car brands in the last few years has already redrawn the landscape, with three Chinese brands now amongst the top 10 best-selling brands in Malaysia, including BYD. Car buyers have also been reaping the benefits of an increasingly competitive market with legacy brands having to cough up sweeter deals (huge discounts in other words) to cope with the aggressive pricing of Chinese automakers.

Put it this way, the Malaysian car market is never going back to the dark days of the 80s and 90s where the mainstream choice is limited to either a Proton/Perodua or paying almost double to get a Japanese equivalent. We now have more options than ever, and we are getting more value for money as well.

What about BYD having to export 80% of its capacity?

The decision to invest in a new plant (hence the manufacturing license) and produce vehicles with high local content is always a tricky one, particularly so in the ASEAN region where governments ‘compete’ by doling out incentives to attract major manufacturers. Long-time players in the region such as Toyota, Honda, BMW, and Mercedes-Benz have mastered the art of pooling resources, being nimble and spreading their investments across key ASEAN markets.

In BYD’s case and according to MITI, the interim manufacturing license was granted “on the basis of an export-oriented production profile, where the majority of output is destined for international markets…”, with the additional condition of an approved domestic sales volume of 10,000 units, or 20% of BYD’s production capacity.

While MITI emphasises that this “is not a restriction but a mutually agreed production framework”, the export component complicates BYD’s endeavour in that it already has plants in Thailand and Indonesia capable of exporting vehicles.

ALSO READ: BYD opens EV factory in Thailand, its first ever in Southeast Asia

Why now and what’s changed since last August?

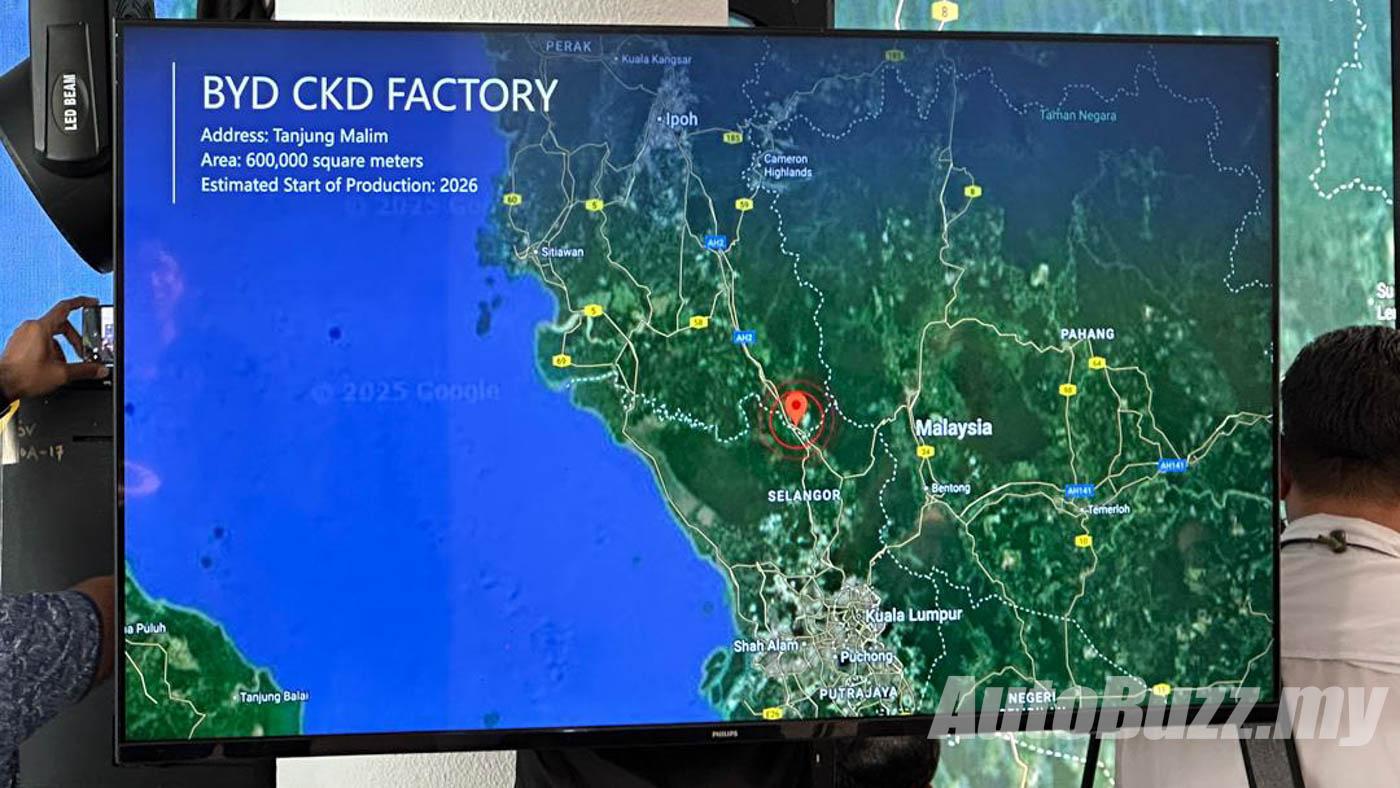

Yet it is important to point out that the framework was mutually agreed by both parties, as MITI asserted. In August last year, BYD announced to the media concrete plans to set up a wholly owned 600,000-square metre factory located at the KLK TechPark in Tanjong Malim. In fact, a report by Malay Mail even mentioned that work on the site had already commenced in July 2025. MITI also clarified that the interim manufacturing license for BYD was then approved on 29 September 2025.

If this is the case, what exactly happened since? What was promised to BYD? Did the terms change? Are there external factors at play? Who leaked this?

While our TIV has been robust in the last few years, the Malaysian Automotive Association is forecasting a contraction of 3.8% for 2026, this is before conflict erupted in the Middle East, so the best laid plans can be derailed by external factors. Maybe the smarter play is to leverage on the manufacturing capacity of the existing ecosystem instead of building another new plant. MITI has also described its policies to be ‘developmental’ and it does leave room for BYD to smooth over the speed hump. We say watch this space.