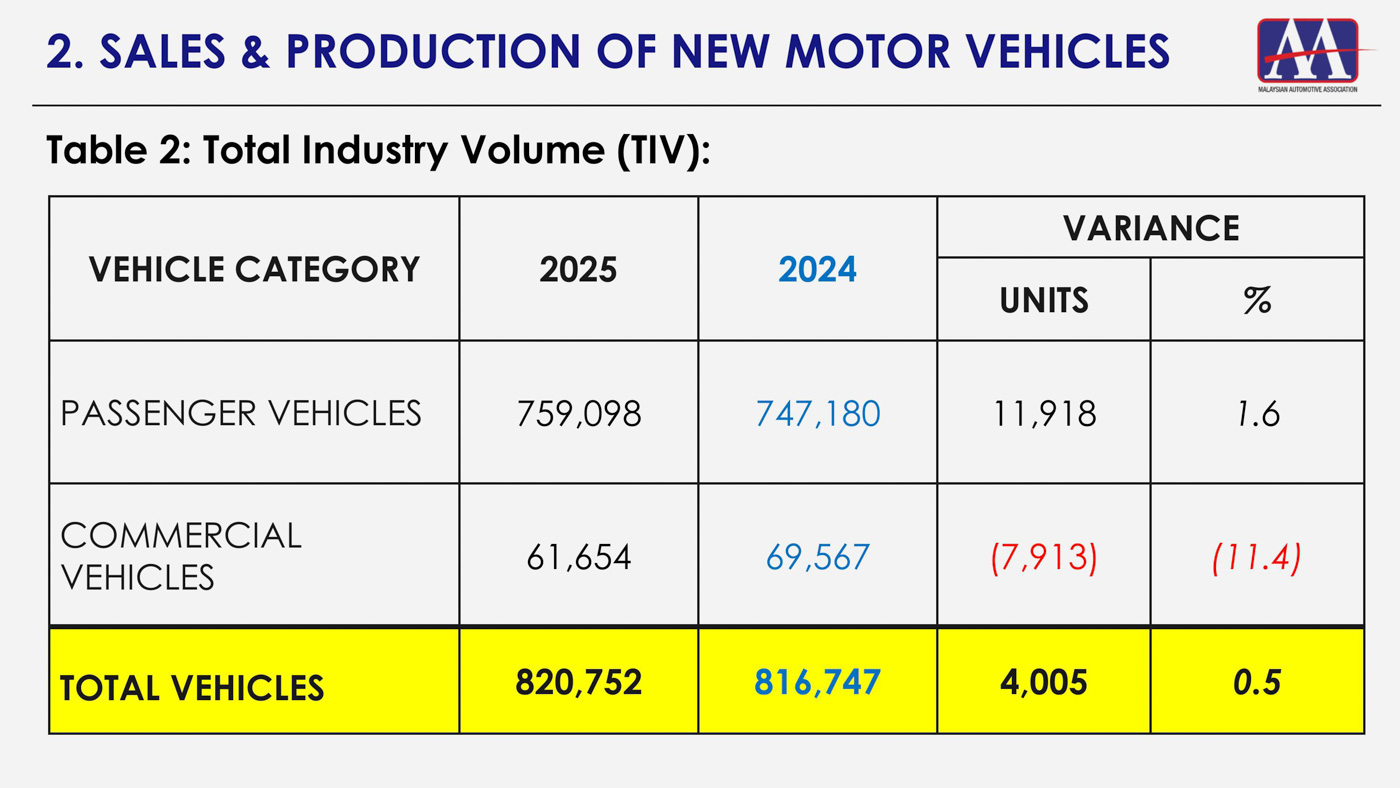

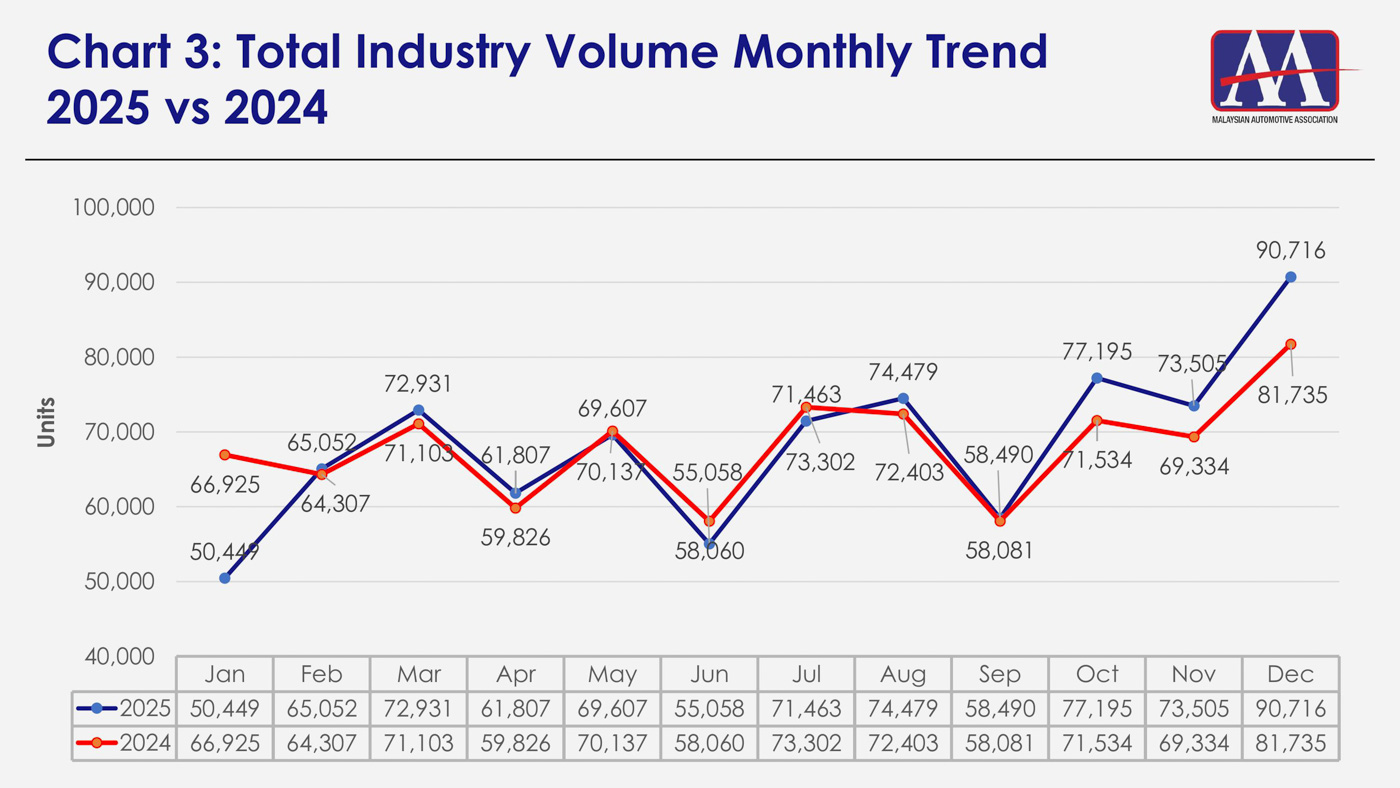

The Malaysian Automotive Association (MAA) reported that a total of 820,752 new vehicles were sold in Malaysia in 2025. This represents a marginal 0.5% increase from the 816,747 units moved in 2024, and marks the second consecutive year the total industry volume (TIV) has exceeded the 800,000-unit threshold.

The year peaked in December with a historic 90,716 units sold – an all-time high monthly figure. Remarkably, this was the first time since December 2024 that the monthly TIV has exceeded the 80,000-unit mark.

MAA attributed these record-breaking numbers to robust economic growth, with Malaysia’s GDP expanding by 4.7% over the first three quarters of 2025. This was bolstered by a favourable lending landscape after the overnight policy rate (OPR) was cut to 2.75% in July. Market conditions were further aided by a stable socio-political environment and a thriving labour market, where unemployment hit an 11-year low of 2.9%.

On the showroom floor, growth was sustained by a strong backlog of orders in the A-segment, from national makes, Proton and Perodua. This momentum was spurred by the rapid adoption of electrified vehicles (xEV), which saw total sales jump 52% to reach 69,363 units.

Among these, the battery electric vehicle (BEV) segment recorded a staggering 109% increase to 30,848 units. The growth spurt was largely driven by a year-end frenzy as buyers rushed to register fully imported (CBU) models before the tax exemptions for CBU BEVs expired on 31 December 2025. Meanwhile, hybrid electric vehicles (HEVs) recorded a growth of 25%, reaching 38,515 units.

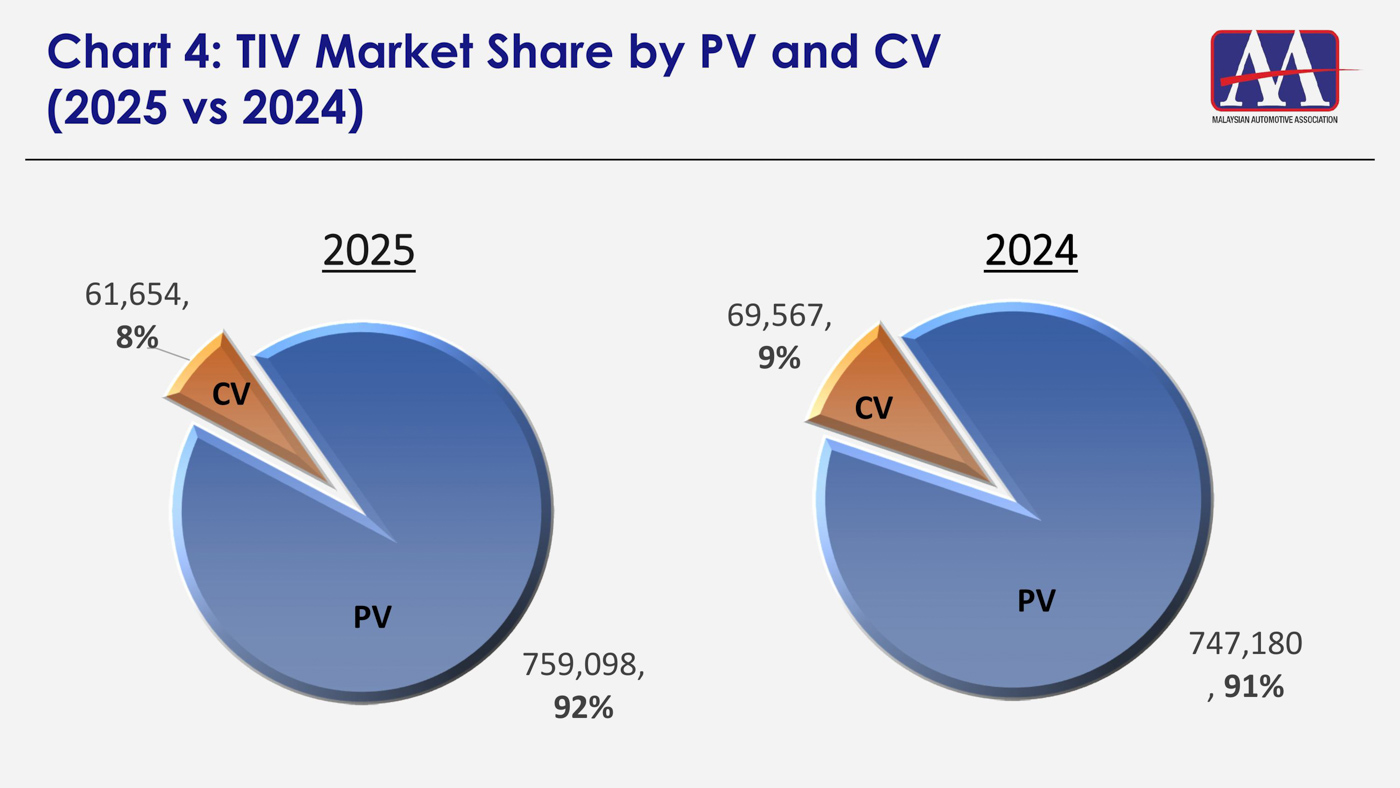

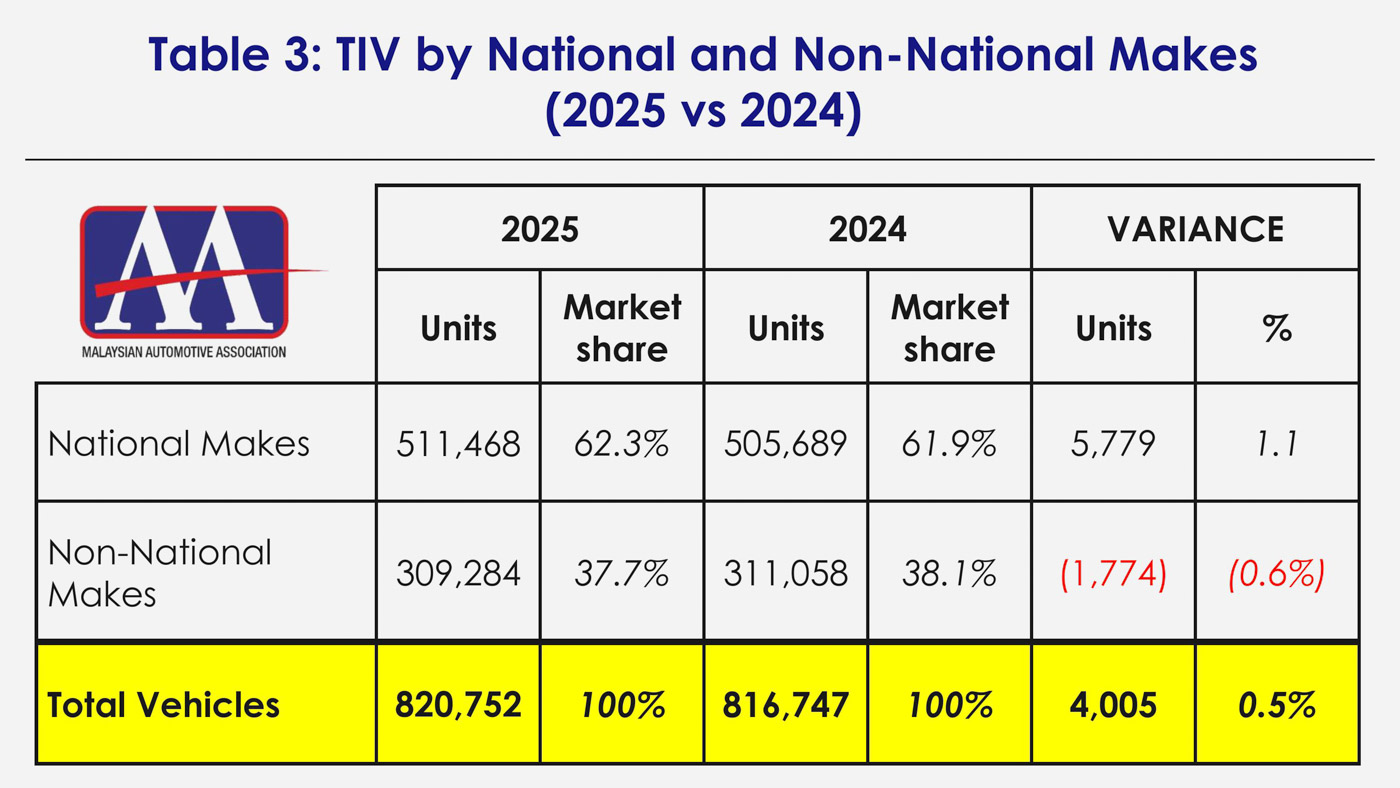

In terms of market share, the two national makes commanded 62.3% of the total market in 2025 with 511,468 units sold. This marks a slight 1.1% gain in market share from 2024. Conversely, non-national makes accounted for 309,284 units, representing a 37.7% share. This 0.6% decline in volume was primarily due to a weaker contribution from the commercial vehicle segment.

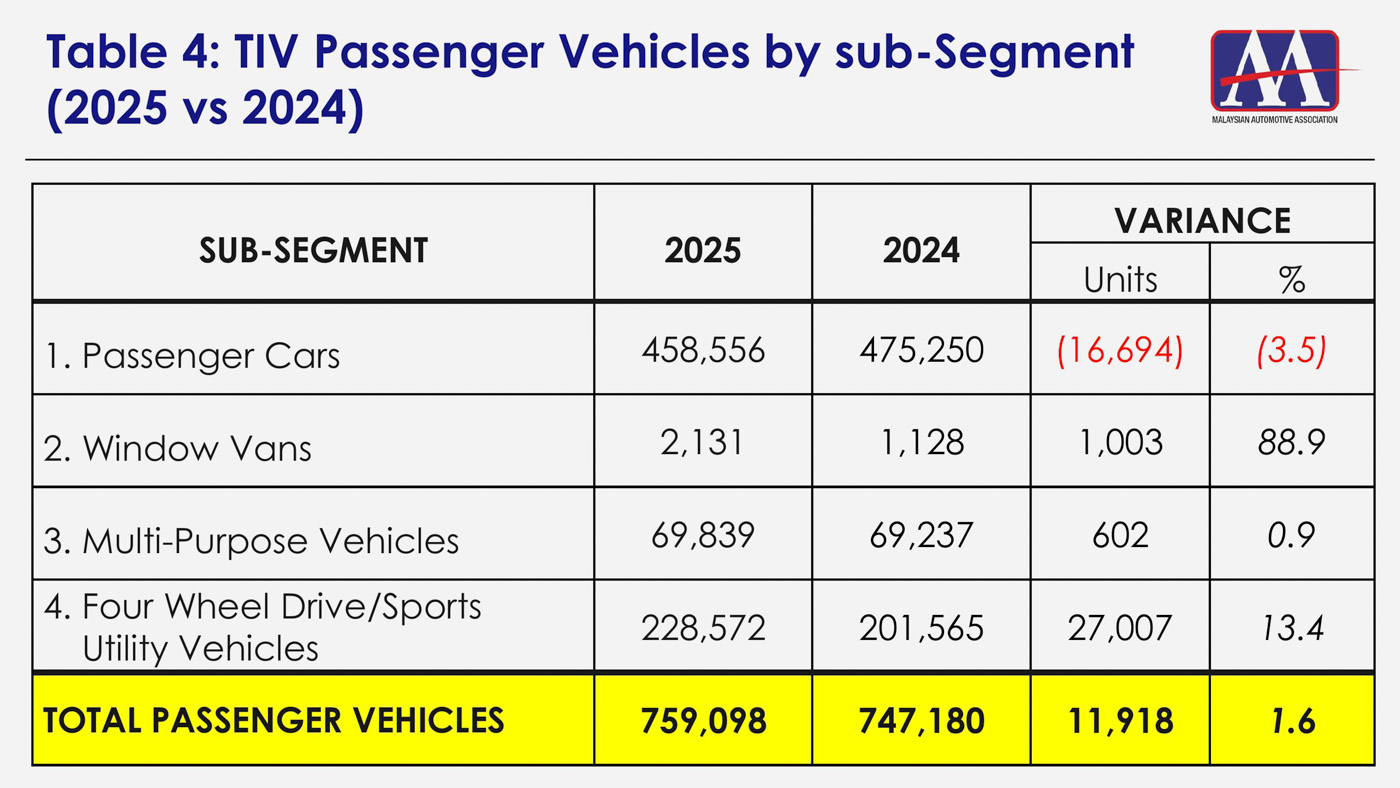

In total, passenger vehicles accounted for 759,098 of the units sold in 2025, a 1.6% increase over 2024. This was largely driven by a significant appetite for SUVs, which saw sales surge by 13.4% to 228,572 units.

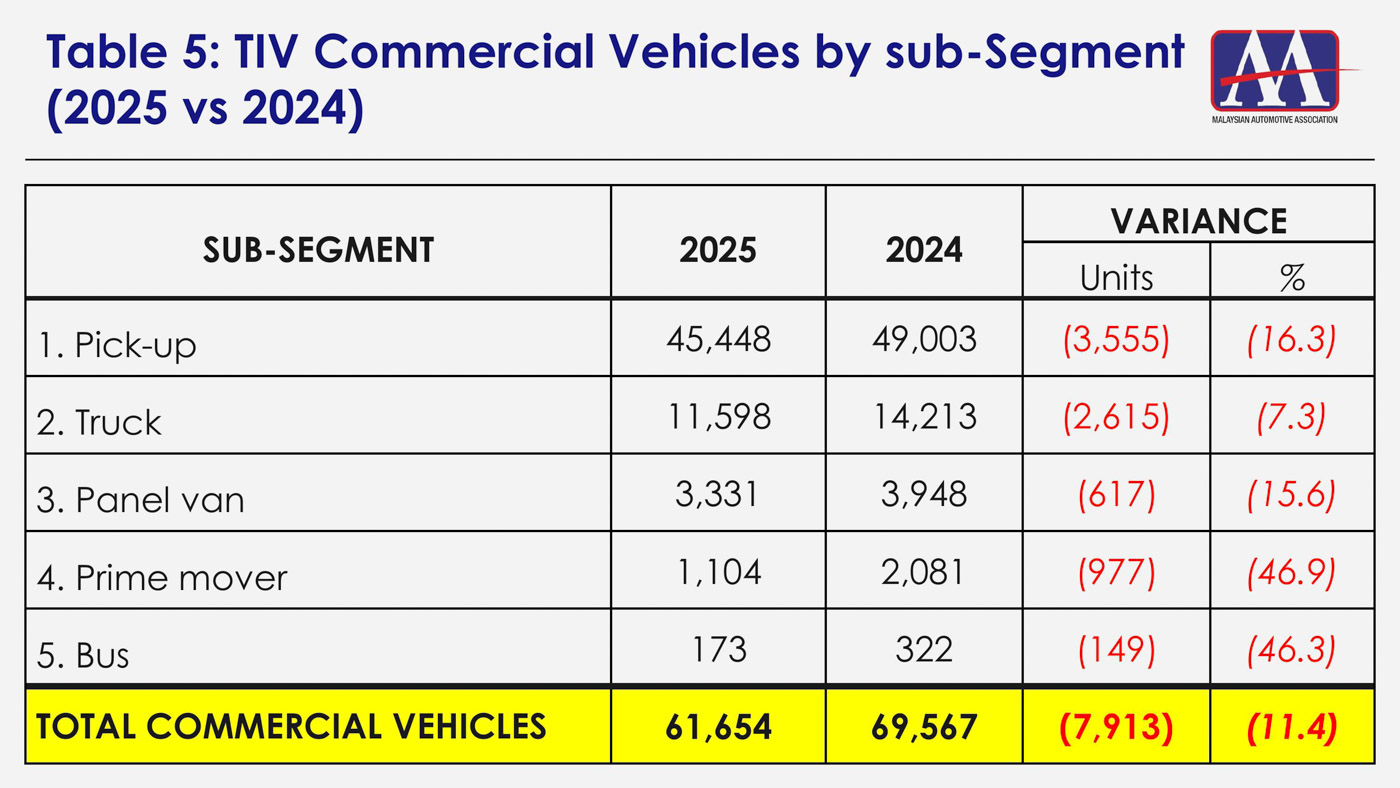

Conversely, the commercial vehicle segment struggled, with sales falling 11.4% to 61,654 units, marking the second consecutive year of declining demand for commercial hauliers.

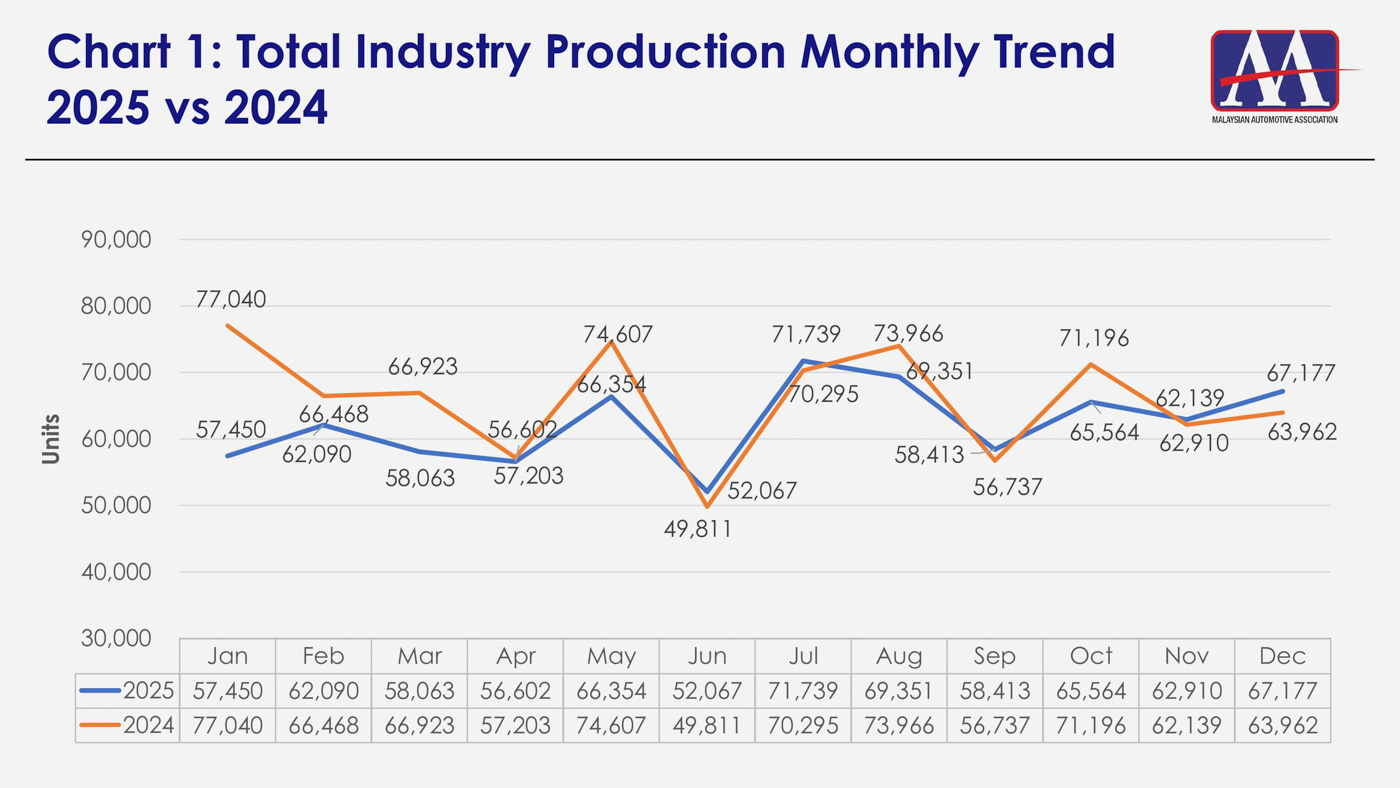

However, while showrooms were busy, local assembly lines were notably quieter. Total Industry Production (TIP) recorded 747,780 units in 2025, representing a 5% decline compared to the 790,347 units produced in 2024.

In a more detailed breakdown, passenger vehicle production fell 5.4% to 704,603 units, while commercial vehicle output dropped 5.6% to 43,177 units. This discrepancy directly reflects the high volume of imported BEVs registered during the year-end rush.

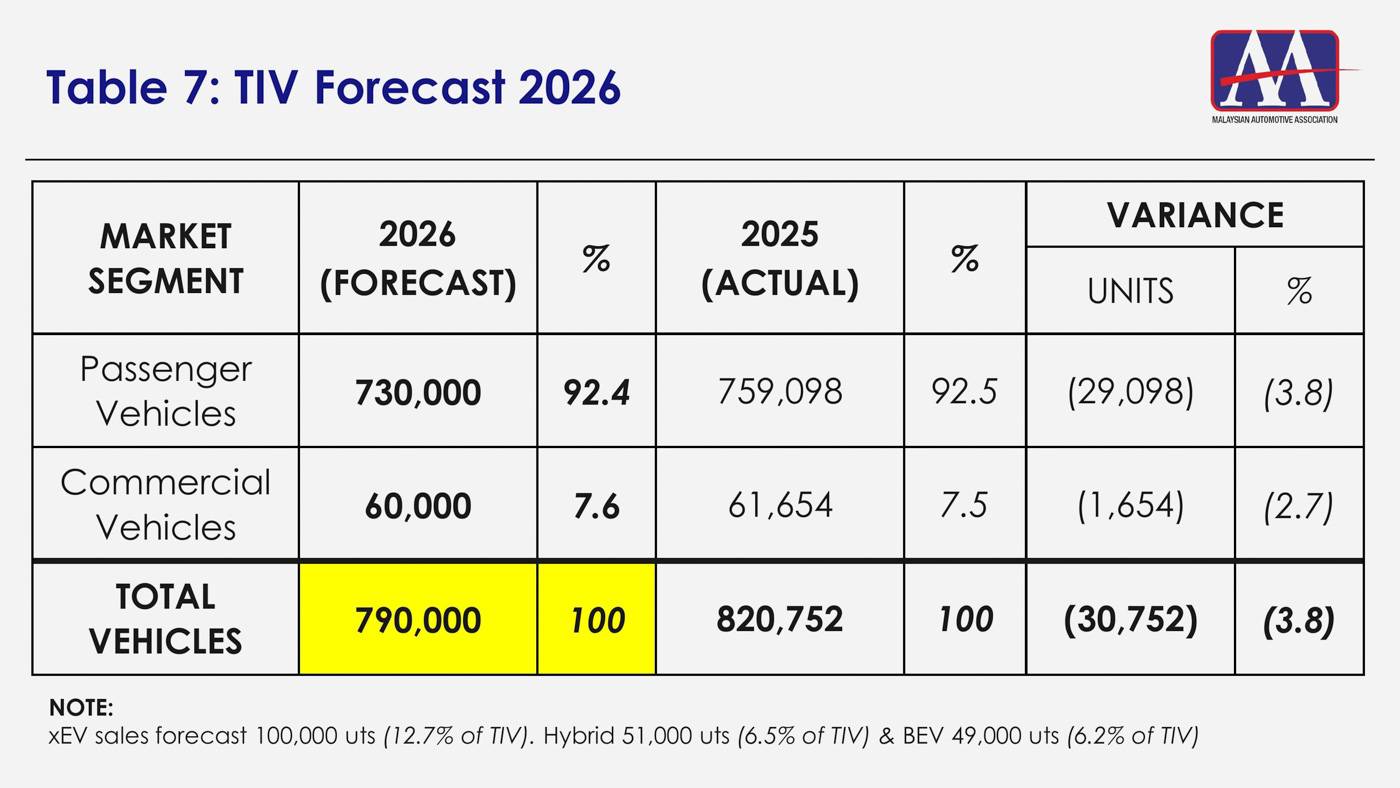

Looking ahead to 2026, the MAA predicts a slight downturn, with TIV forecast to settle at 790,000 units. This cautious outlook is due to moderate GDP growth, global trade uncertainties, and persistent inflationary pressures. Other challenges include the rationalisation of RON95 petrol subsidies and the rising cost of living.

GALLERY